A better way for the Federal Government to financially support Licensed Live Music Venues and Festivals in crisis is by an Alcohol Excise and Wine Equalisation Tax rebate scheme.

Prior to March 2020, when the COVID pandemic hit, the Live Music Industry was growing economically as a sector. Like many industries, it had its headwinds and distortions, but nothing could prepare it for what would come.

The sector got well and truly smashed by the lockdowns. It was affected more than any other sector of the economy, and the pronounced Morison “Snapback” never happened. Post-Covid, inflation spiked, and operating costs like public liability insurance ballooned, whilst audiences and the number of active bands halved. The details of the damage are extensive, which I will detail in another forthcoming article. However, the economic and cultural damage to the sector is widely accepted.

Federal and State Governments responded with their standard toolset: Grants.

However, these tools are competitive, ad-hoc, over-subscribed, and require substantial resources and skills to apply for them. The criteria often steer the grant funds into activities that are not critical to the organisation's survival. Whereas Live Music Venues' financial priorities are core fixed costs such as rent, property costs, permanent staff costs, public liability insurance, etc. Many festivals and venues also carry substantial debt accumulated during the lockdowns, which grants specifically can not be directed to addressing.

Examples include grants such as RISE, Live Music Australia, Revive and The Victoria Government's 10,000 gigs program. They mainly target equipment upgrades, training and programming costs. Program-orientated grants do little to reverse venue trading losses and, therefore, result in gig losses. Whereas correctly targeted assistance to struggling venues’ core operating costs will save live music venues and the gigs they host.

What live music venues desperately need is a direct injection of money into their working capital. Without this, live music venues and festivals will continue on a trajectory of economic attrition and sector contraction.

Saving a single live music venue from closure would equate to saving about 780 live music shows over the 4-year life of the program. This equated to 2,345 band gigs assuming three band line-ups. These are shows that would otherwise be lost.

Financial assisting and saving live music venues from closure would have a more significant and enduring impact than existing ad-hoc program funding grants.

This is further backed up by one of the recommendations of Music Victoria’s 2022 Victoria Live Music Census,

“That the state government extend the live music venue support grants to assist small venue operators to refurbish infrastructure and restore the viability of their operations and to reinvigorate our famous live music scene.”

Although this recommendation was directed at the Victorian State Government, it is equally relevant to Federal Government policy as the industry contributes annually in excess of $15.7 billion to the economy and sustains 60,000 jobs. The cultural damage being done to live music will be long lasting unless Government acts! Every $1 spent on live music leverages $3 in the economy.

https://livemusicoffice.com.au/research

The disproportionate tax burden.

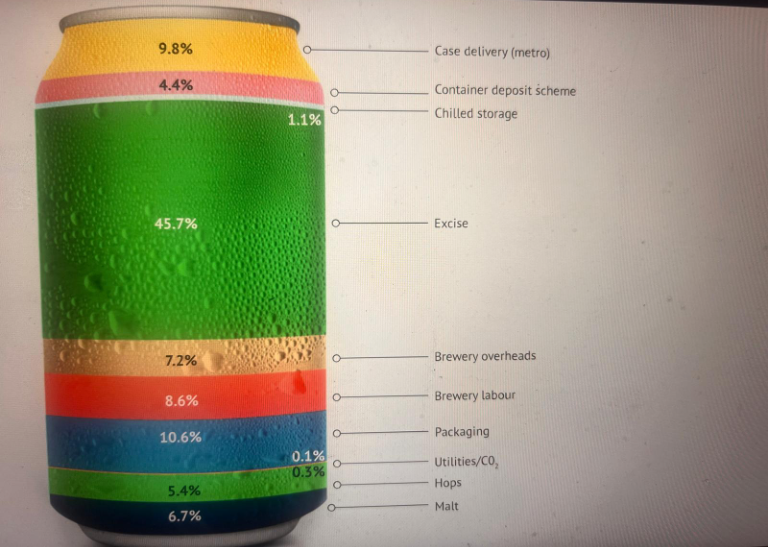

Live Music Venues pay more tax, levies and licencing fees than almost any other sector of the economy. These taxes include the Wine Equalisation Tax, Alcohol Excise, Liquor License Fees, Land Tax (either directly or indirectly through rent), PAYG, Payroll Tax, Council Rates, Heath Licenses, Fire levies, GST, water and waste charges, and Company Tax. Although not a tax, live music venues and festivals are also responsible for paying OneMusic music copyright license fees.

Brewer costs of Beer. Source: The Age

The Government should consider that if licenced live music venues and festivals fail or cease operation, then this is enduring taxation revenue that the government would not otherwise raise.

A Proposal for an Alcohol Excise and Wine Equalisation Tax rebate scheme for hospitality-based Live Music Venues and Festivals to facilitate financial recovery from Covid-related economic damage.

This is a simple proposal that would be easy to implement by the Federal Government, would address struggling hospitality-based small to medium live music venues and licensed festivals, offset core costs and is likely to be revenue neutral.

This proposal is for a system of Alcohol Excise and Wine Equalisation Tax rebates for Live Music Venues and Festivals that hold liquor licenses. The Federal Government could create a rebate scheme on alcohol excise and the Wine Equalisation Tax (WET) currently collected by the Federal Government that would only be available to legitimate licensed grassroots live music venues and small live music festivals. It would not need to be permanent and would only need to last for a set recovery period (say 4 years) to assist these culturally vital organisations in recovering from the COVID lockdown's enduring financial impacts.

This would be achieved by targeting their critical financial problem of lack of profitability in the current post-COVID ramp-up recovery period when they are carrying the added weight of accumulated COVID debt generated during and after the lockdown whilst they are operating at substantially reduced income levels.

It could operate as follows:

• Eligibility would be specific to small to medium live music venues and music festivals under 10,000 capacity who hold both a valid liquor license and a OneMusic license covering live music royalty collection. Also, a documented history of staging live music or other performance activity, such as comedy, by presenting records of door reconciliation sheets, OneMusic live music reports or other proof of live music programming. The eligibility criteria for this rebate proposition are simple and have already been utilised by the Live Music Australia Grants.

• Alcohol excise is based on alcohol volumes, not sales value but can easily be accounted for by licensed Live music venues and festivals. The summation of alcohol purchase quantities organised by the Excise Tariff sub-item category could easily form the basis of the rebate calculations by using invoices for stock from the licensed Live music venues or festivals suppliers as the documentary evidence basis to a validate rebate claims.

• The WET is based on 29% of the wholesale price of wine so the invoiced amount from licensed live music venues or festivals suppliers would also suffice for a claim with invoices forming the evidence base.

Although there is an administrative overhead for this scheme, this is well outweighed by the beneficial financial impact of the proposal. The rough value of alcohol excise represents around 12% to 15% (25% COG of 46% wholesale excise) of a live music venue’s turnover. This would turbocharge the profitability of legitimate small to medium live music venues and festival bar sales. The increased cash flow would address the disproportionate operating costs caused by accumulated COVID lockdown debt and other disproportionate inflationary headwinds such as the massive increases in public liability insurance.

Although a direct injection of working capital into live music venues and festivals by the Government is an alternative through correctly targeted grants, this rebate proposition would equally work to specifically address live music venues and festivals’ future economic needs and underpin musician employment sustainability.

Implementation of this proposal by the Government would not require any new or amended legislation in parliament.

This proposal also aligns with the proposal by APRA/AMCOS for a Live music tax offset.

The report prepared by BIS Oxford Economics indicated that sector-wide support for live music would be as follows:

• The BISOE report found that a tax offset would incentivise existing live music venues to host more live performances and enable non-live music venues to host live music performances.

• A combined venue offset (of 5% of expenses for current live music venues and $12,000 in expenses for those not currently hosting) would boost the incomes of musicians and artists by $205 million per year with an additional 203,200 gigs.

• Such a combined offset could also support 7,400 direct and indirect jobs across entertainment, hospitality and tourism, and contribute $636 million per annum to Gross Value Added (GVA).

• The tax offset would boost annual industry GVA by between $310 million (i.e. an increase of approximately 10%) and $495 million (an increase of 15%); andcontribute to employment by between 3,600 (an increase of 10%) and 5,800 jobs (an increase of 15%), depending on the scenario modelled.

• A key motivation of the offsets is to encourage a healthy live performance ecosystem.

Apart from establishing a vibrant cultural life in Australia’s cities and rural centres and enhancing quality of life, supporting live music may also provide other long-term benefits such as enhancing Australian musical exports and soft power.

Although the APRA/AMCOS/BISOE report did not consider this Alcohol Excise and Wine Equalisation Tax rebate proposed, the report specifically did not specify the mechanics of how a tax offset for live music could be implemented.

https://www.apraamcos.com.au/about/supporting-the-industry/research-papers/economicimpact-of-tax-offsets-on-the-live-music-industry

https://assets.apraamcos.com.au/images/PDFs/About/APRA-OE-Report-Tax-IncentivesFINAL-REPORT.pdf

Precedents

There are precedents for such an initiative. The three examples given show that such an excise rebate scheme is not novel and is viable. Although the jurisdictions and scheme’s scope vary, they do offer benchmarks for the establishment and implementation of this proposal.

Further research would result in a more extensive list.

The Victorian Government established the Community Support Fund (CSF)

In 1991, The Victorian Government established the Community Support Fund (CSF). It is a trust fund governed by the Gambling Regulation Act 2003 to direct a portion of gaming revenue back to the community.

As prescribed by the legislation, the CSF receives 8.33 per cent of the revenue generated from the operation of electronic gaming machines in hotels. Any investment interest earned on the fund is retained and distributed for the community purposes set out in the legislation, including arts and tourist based initiates and funding of support or advancement of the community as determined by the Minister.

In 2019-20, the CSF received $112.23 million in revenue. This was lower than expected due to the COVID-related public health restrictions.

https://www.dtf.vic.gov.au/funds-programs-and-policies/community-support-fund

Other examples of alcohol excise rebates being redirected to live music include:

Texas Music Incubator Rebate Program (Austin, Texas, USA)

The Texas Music Incubator Rebate Program allows live music venues in Austin to receive up to $100,000 annually in liquor tax rebates. This program was established to provide financial relief to venues that significantly contribute to the live music scene. The Texas Music Office administers the program, which has a total funding of over $10 million for the next two years. To qualify, venues must meet specific criteria related to their operations and the promotion of live music.

https://www.austinmonitor.com/stories/2023/05/austin-music-venues-could-receive-100k-liquor-tax-rebates-from-new-state-incubator/

Proposed Liquor Tax Rebate Program (Cleveland, Ohio, USA)

In Cleveland, a proposal has been introduced to create a live music fund using liquor taxes collected from venues with a capacity of 3,000 people or less. If approved, this program would allow these venues to apply for rebates of up to $100,000 annually, with a total cap of $10 million for the initiative. This proposal aims to support the local music industry and enhance the cultural landscape of the region

https://www.wosu.org/2024-08-29/ohio-lawmakers-propose-liquor-taxes-to-support-live-music-venues-at-rock-hall

In conclusion

As Live Music Venues and Music Festival employ and contract a substantial proportion of Australian bands and musicians, Live Music Venues and Festivals are the important economic scaffold for musicians and music workers to sustain their careers. This is particularly true for emerging and developing musicians and bands.

Live music venues and festivals are the creative cauldron of the music industry's 60,000 jobs. The federal government has historically under-invested in contemporary live music compared to other industries of similar size, and even in terms of the shrinking arts funding pool.

As such, this proposal will likely be close to revenue neutral, representing a sound and wise investment by the Federal Government in the Live Music industry and the future of Australian musical culture.

Jon Perring

This article was part of a submission to the Standing Committee on Communications and the Arts into The challenges and opportunities within the Australian live music industry written by Jon Perring on the 12th of April 2024 and was also submitted to the Parliament of Australia’s enquiry into “Australia’s creative and cultural industries and institutions” titled “A proposal for an Alcohol Excise and Wine Equalisation Tax rebate scheme for Live Music Venues and Festivals to address the sectors future financial sustainability and COVID pandemic recovery” on the 1st October 2020 by Jon Perring.

An earlier version was also submitted as part of a submission to the National Cultural Policy (https://www.arts.gov.au/sites/default/files/documents/ncp0508-the-tote-hotel-and-baropen.pdf).